A degenerate gambler down on his luck. No matter how carefully he placed his bets, he always seemed to come up short. One day, he heard about a race with only one horse in it. It seemed like a sure thing, a chance to finally turn his fortunes around. So, he took all the money he had set aside for rent and put it on this lone horse.

The race began, and the gambler watched with anticipation as the horse took off from the starting gate. But halfway around the track, the horse suddenly veered off course, jumped over the fence, and ran away into the countryside.

The gambler was stunned. He had just lost everything on what seemed like the surest bet imaginable.

In all aspects of our lives, we base our decisions on what we think probably will happen. And, in turn, we base that to a great extent on what usually happened in the past. We expect results to be close to the norm (A) most of the time, but we know it’s not unusual to see outcomes that are better (B) or worse (C). Although we should bear in mind that, once in a while, a result will be outside the usual range (D), we tend to forget about the potential for outliers.

Things can always get worse than people expect. We often measure risk as the “worst-case scenario” - the worst thing that’s happened in the past. But the future has a way of surprising us. Just because something hasn’t happened before doesn’t mean it can’t happen in the future.

In investing, this principle is especially important. Markets are complex and unpredictable, and the past is not always a reliable guide to the future. Just because a particular investment or strategy has worked well historically doesn’t guarantee it will continue to do so.

That’s why Howard Marks, in his book “The Most Important Thing,” emphasizes the importance of understanding and managing risk in investing. Marks argues that successful investing is not just about pursuing returns; it’s also about controlling risk and preparing for the unexpected.

Through his insights and examples, Marks shows how investors can navigate the uncertainties of the market by focusing on key principles of risk management.

- What did I get out of it?

- Who Should Read It?

What did I get out of it?

The Most Important Thing, by Howard Marks is a book on risk management, particularly when it comes to financial investments. However, risk management doesn’t have to be confined to investments, the lessons in the book are timeless and you can easily draw parallels and apply these principles to other areas of your life too, be it health, career or relationships.

Reading this book helped me refine my own risk management framework. These principles apply not just to financial health, but to all my decisions. I have distilled these lessons into the following categories:

- Understanding and Recognizing Risk

- Second-level Thinking

- Understanding the Environment

- Margin of Safety

- Circle of Competence

Understanding and Recognizing Risk

Marks hammers home the point that risk is often hidden, lurking in the shadows when everyone thinks the coast is clear. It’s like a game of hide-and-seek, but with much higher stakes. The key is to train yourself to spot risk when others are oblivious to it. When everyone’s feeling confident and the markets on a hot streak, that’s when you need to be extra cautious.

Defining Risk

The first step consists of understanding it. The second step is recognizing when it’s high. The critical final step is controlling it.

Whether you’re making a career decision, entering a new relationship, or embarking on a major life change, understanding the risks involved, recognizing when those risks are elevated, and know your response to these uncertainties.

…only when investors are sufficiently risk-averse will markets offer adequate risk premiums. When worry is in short supply, risky borrowers and questionable schemes will have easy access to capital, and the financial system will become precarious. Too much money will chase the risky and the new, driving up asset prices and driving down prospective returns and safety.

However, risk is unavoidable. Hence, to understand you must know what you can stomach before throwing up.

Investing consists of exactly one thing: dealing with the future. And because none of us can know the future with certainty, risk is inescapable. Thus, dealing with risk is an essential—I think the essential—element in investing.

Volatility vs True Risk

Before we go any further, you must understand that what we call risk in theory and what makes you throw up are two different things. Academics refer to volatility as risk. Does volatility make you throw up?

According to the academicians who developed capital market theory, risk equals volatility, because volatility indicates the unreliability of an investment. I take great issue with this definition of risk. It’s my view that—knowingly or unknowingly—academicians settled on volatility as the proxy for risk as a matter of convenience.

Volatility is a poor proxy for true investment risk. Just because an asset’s price is volatile doesn’t necessarily mean that it’s fundamentally risky or that it’s a bad investment. In fact, some of the most successful investors in history have made their fortunes by embracing volatility and using it to their advantage.

This idea has implications beyond just investing. In many areas of life, we often rely on convenient but imperfect proxies for complex concepts like risk, success, or happiness. By challenging these assumptions and thinking more deeply about what truly matters, we can make better decisions and live more fulfilling lives.

But just because something is easy to measure doesn’t mean it’s the right thing to measure.

The problem with all of this, however, is that I just don’t think volatility is the risk most investors care about. There are many kinds of risk…. But volatility may be the least relevant of them all. Theory says investors demand more return from investments that are more volatile. But for the market to set the prices for investments such that more volatile investments will appear likely to produce higher returns, there have to be people demanding that relationship, and I haven’t met them yet.

Rather than relying on simplistic measures like volatility, you should strive to understand the specific risks that are most relevant to your own situation and goals.

The importance of independent thinking and a willingness to challenge conventional wisdom in investing and decision-making.

Rather than volatility, I think people decline to make investments primarily because they’re worried about a loss of capital or an unacceptably low return.

Intuitively we can all agree that we are not really concerned with volatility of the stock prices, but the risk of losing our capital.

…loss is what happens when risk meets adversity. Risk is the potential for loss if things go wrong. As long as things go well, loss does not arise. Risk gives rise to loss only when negative events occur in the environment.

Risk is the potential for loss. It’s always present, even when things are going well.

The possibility of permanent loss is the risk I worry about…

Measuring Risk

If volatility is not risk, so how do we measure risk?

There is inherent difficulty in quantifying risk because everyone looks at risk differently.

Quantitative risk measures like volatility or beta can be useful inputs, they don’t tell the whole story. You must also consider qualitative factors.

…the standard for quantification is nonexistent. With any given investment, some people will think the risk is high and others will think it’s low. Some will state it as the probability of not making money, and some as the probability of losing a given fraction of their money (and so forth). Some will think of it as the risk of losing money over one year, and some as the risk of losing money over the entire holding period. Clearly, even if all the investors involved met in a room and showed their cards, they’d never agree on a single number representing an investment’s riskiness. And even if they could, that number wouldn’t likely be capable of being compared against another number, set by another group of investors, for another investment.

It requires a combination of analytical rigor and sound judgment. While quantitative risk measures can be useful inputs, they are no substitute for a deep understanding of the underlying drivers of value and a well-reasoned assessment of the potential risks and rewards.

Saying that, it may be relatively easy to account for and quantify conventional, frequently occurring risks. You can look at historical data, identify patterns, and make reasonable estimates of the likelihood and potential impact of these risks.

Financial institutions routinely employ quantitative “risk managers” separate from their asset management teams and have adopted computer models such as “value at risk” to measure the risk in a portfolio. But the results produced by these people and their tools will be no better than the inputs they rely on and the judgments they make about how to process the inputs. In my opinion, they’ll never be as good as the best investors’ subjective judgments.

Sharpe ratio. This is the ratio of a portfolio’s excess return (its return above the “riskless rate,” or the rate on short-term Treasury bills) to the standard deviation of the return. This calculation seems serviceable for public market securities that trade and price often; there is some logic, and it truly is the best we have. While it says nothing explicitly about the likelihood of loss, there may be reason to believe that the prices of fundamentally riskier securities fluctuate more than those of safer ones, and thus that the Sharpe ratio has some relevance. For private assets lacking market prices—like real estate and whole companies—there’s no alternative to subjective risk adjustment.

It stands to reason that most risk is measured using qualitative assessment.

While Sharpe ratio can be a useful data point for measuring risk for listed securities, it has very limited applications.

…while considering the difficulty of measuring risk prospectively, I realized that because of its latent, nonquantitative and subjective nature, the risk of an investment—defined as the likelihood of loss—can’t be measured in retrospect any more than it can a priori.

Unless you think future, risk events will be of the same magnitude as those in the past, the quantitative models relying on historical data cannot reflect true risk.

…risk is deceptive. Conventional considerations are easy to factor in, like the likelihood that normally recurring events will recur. But freakish, once-in-a-lifetime events are hard to quantify. The fact that an investment is susceptible to a particularly serious risk that will occur infrequently if at all—what I call the improbable disaster—means it can seem safer than it really is.

The real danger often lies in “the improbable disaster” - rare, catastrophic events that are difficult to predict or quantify. These might include things like natural disasters, geopolitical shocks, or sudden market crashes.

This is a classic example of the “turkey problem” described by Nassim Nicholas Taleb. A turkey that is fed every day may come to believe that its life is safe and predictable, not realizing that it is being fattened up for Thanksgiving. In the same way, you can be lulled into a false sense of security by extended periods of stable returns, only to be blindsided when a rare but severe event strikes.

…failure of imagination consists in the first instance of not anticipating the possible extremeness of future events, and in the second instance of failing to understand the knock-on consequences of extreme events.

You cannot measure such a risk. This is qualitative and subjective assessment.

Quantification often lends excessive authority to statements that should be taken with a grain of salt. That creates significant potential for trouble.

Ultimately, recognizing the limits of quantification is an essential part of understanding and managing risk in an uncertain world.

Identifying the Hidden Risk

Another major problem in understanding and measuring risk is that much of it is hidden, as the concept of many possible outcomes isn’t intuitive.

The fact that something—in this case, loss—happened doesn’t mean it was bound to happen, and the fact that something didn’t happen doesn’t mean it was unlikely.

We often fall prey to hindsight bias, seeing past events as predictable or obvious, even if they were not. When an investment loses money, it’s easy to look back and conclude that the loss was inevitable, given the risks involved. But this ignores the fact that other, more favorable outcomes were also possible, even if they did not come to pass.

Similarly, when an investment performs well, we may be tempted to conclude that the positive outcome was a sure thing, and that the risks were lower than they actually were. But this fails to account for the role of chance and the potential for things to have turned out differently.

We must remember that when the environment is salutary, that is only one of the environments that could have materialized that day (or that year). The fact that the environment wasn’t negative does not mean that it couldn’t have been. Thus, the fact that the environment wasn’t negative doesn’t mean risk control wasn’t desirable, even though—as things turned out—it wasn’t needed at that time.

Ultimately, successful investing requires a keen understanding of the interplay between probability and outcome. By recognizing that what happened was not necessarily bound to happen, and that what did not happen was not necessarily unlikely, you can make more nuanced and effective decisions in the face of uncertainty.

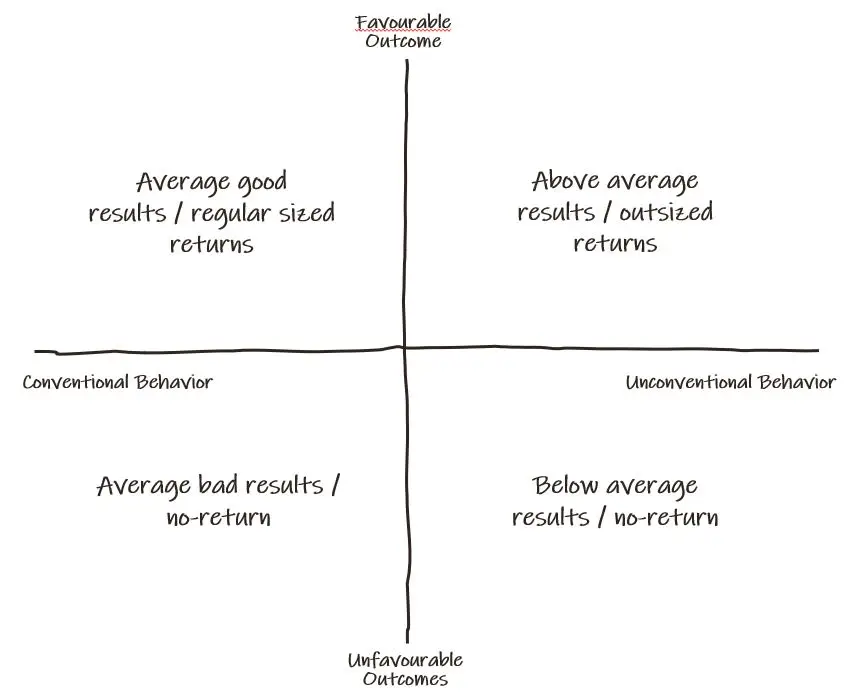

In the investing world, one can live for years off one great coup or one extreme but eventually accurate forecast. But what’s proved by one success? When markets are booming, the best results often go to those who take the most risk. Were they smart to anticipate good times and bulk up on beta, or just congenitally aggressive types who were bailed out by events? Most simply put, how often in our business are people right for the wrong reason? These are the people Nassim Nicholas Taleb calls “lucky idiots,” and in the short run it’s certainly hard to tell them from skilled investors. The point is that even after an investment has been closed out, it’s impossible to tell how much risk it entailed. Certainly the fact that an investment worked doesn’t mean it wasn’t risky, and vice versa. With regard to a successful investment, where do you look to learn whether the favorable outcome was inescapable or just one of a hundred possibilities (many of them unpleasant)? And ditto for a loser: how do we ascertain whether it was a reasonable but ill-fated venture, or just a wild stab that deserved to be punished? Did the investor do a good job of assessing the risk entailed?

Evaluating performance in any domain subject to chance and uncertainty. In fields ranging from business to sports to the arts, it can be easy to confuse luck with skill, or to draw overly strong conclusions from a small sample of outcomes.

The understanding of many worlds concept helps us understand hidden risk and uncertainty.

Investing consists of exactly one thing: dealing with the future. Yet clearly it’s impossible to “know” anything about the future. If we’re farsighted we can have an idea of the range of future outcomes and their relative likelihood of occurring—that is, we can fashion a rough probability distribution. (On the other hand, if we’re not, we won’t know these things and it’ll be pure guesswork.) If we have a sense for the future, we’ll be able to say which outcome is most likely, what other outcomes also have a good chance of occurring, how broad the range of possible outcomes is and thus what the “expected result” is. The expected result is calculated by weighting each outcome by its probability of occurring; it’s a figure that says a lot—but not everything—about the likely future.

Developing probabilistic thinking can help us. Rather than focusing on a single predicted outcome, considering a full range of possibilities and their associated probabilities can broaden our perspective.

All the same, this approach has its pitfalls as well due to limits of our foresight.

“There’s a big difference between probability and outcome. Probable things fail to happen—and improbable things happen—all the time.” That’s one of the most important things you can know about investment risk.

Hence, we can never estimate and quantify the risk entirely. What we can do is stay humble and open minded. No matter how confident we may be in our predictions or beliefs, there is always a chance that things could turn out differently than our expectations.

Many futures are possible, to paraphrase Dimson, but only one future occurs. The future you get may be beneficial to your portfolio or harmful, and that may be attributable to your foresight, prudence or luck. The performance of your portfolio under the one scenario that unfolds says nothing about how it would have fared under the many “alternative histories” that were possible.

Ultimately, risk and luck are two sides of the same coin.

Second-level Thinking:

In this section, we explore the one key skill required to be a good risk manager.

Beyond First-level Thinking

Marks argues that successful investors don’t just take things at face value. They dig deeper, considering all the angles and possibilities. It’s like playing chess: you can’t just think about your next move; you have to anticipate your opponent’s moves and plan several steps ahead. In investing, that means looking beyond the obvious and considering factors like probability distributions, market consensus, and potential outcomes.

First-level thinking is simplistic and superficial, and just about everyone can do it (a bad sign for anything involving an attempt at superiority). All the first-level thinker needs is an opinion about the future, as in “The outlook for the company is favorable, meaning the stock will go up.” Second-level thinking is deep, complex and convoluted. The second-level thinker takes a great many things into account:

• What is the range of likely future outcomes?

• Which outcome do I think will occur?

• What’s the probability I’m right?

• What does the consensus think?

• How does my expectation differ from the consensus?

• How does the current price for the asset comport with the consensus view of the future, and with mine?

• Is the consensus psychology that’s incorporated in the price too bullish or bearish?

• What will happen to the asset’s price if the consensus turns out to be right, and what if I’m right?

You need to dig deeper and consider a wide range of factors that others might be overlooking.

By asking questions like “What’s the probability I’m right?” and “How does my expectation differ from the consensus?”, you can start to develop a more nuanced view of your investments. You’ll be better equipped to spot opportunities that others might miss, and you’ll be less likely to get caught up in market hype or groupthink.

But the implications of second-level thinking go beyond just investing. In any area of life, from career choices to personal relationships, taking the time to think deeply and consider multiple perspectives can lead to better outcomes. It’s about being willing to embrace complexity and uncertainty, rather than always seeking the simplest or most comforting answer.

Being a Contrarian

Of course, second-level thinking isn’t easy. It requires mental discipline, curiosity, and a willingness to challenge your own assumptions.

The problem is that extraordinary performance comes only from correct non consensus forecasts, but non consensus forecasts are hard to make, hard to make correctly and hard to act on.

Even if you do make a non-consensus forecast that turns out to be correct, acting on it can be just as challenging. When everyone else is zigging, it’s tough to zag. There’s a lot of pressure to conform to the crowd, both from external sources like the media and from our own internal biases and doubts.

Of course, that doesn’t mean you should always be a contrarian just for the sake of being different. Not every non consensus view is correct, and not every consensus view is wrong. The key is to do your own research, think critically about what you’re hearing from others, and be honest with yourself about what you do and don’t know.

If you believe the story everyone else believes, you’ll do what they do. Usually you’ll buy at high prices and sell at lows. You’ll fall for tales of the “silver bullet” capable of delivering high returns without risk. You’ll buy what’s been doing well and sell what’s been doing poorly. And you’ll suffer losses in crashes and miss out when things recover from bottoms. In other words, you’ll be a conformist, not a maverick; a follower, not a contrarian.

This is the essence of second-level thinking: being willing to go against the grain in pursuit of exceptional outcomes, even if it means risking underperformance in the short term. It’s about having the conviction to make bold, non-consensus bets based on your own independent analysis and judgment.

Second-level thinkers know that, to achieve superior results, they have to have an edge in either information or analysis, or both. They are on the alert for instances of misperception. My son Andrew is a budding investor, and he comes up with lots of appealing investment ideas based on today’s facts and the outlook for tomorrow. But he’s been well trained. His first test is always the same: “And who doesn’t know that?”

“And who doesn’t know that?” - is a great example of second level thinking in action. It’s a way of forcing yourself to think beyond the obvious and consider whether your investment thesis is really as strong as it seems.

…there are two essential ingredients for profit in a declining market: you have to have a view on intrinsic value, and you have to hold that view strongly enough to be able to hang in and buy even as price declines suggest that you’re wrong. Oh yes, there’s a third: you have to be right.

It’s not just about having a different view from the crowd, but about having a view that is based on a deep understanding of the risks and opportunities. This requires work.

When you do the work, you can look beyond the obvious. The obvious is usually priced in and it’s the non-obvious that must be identified.

…risk of loss does not necessarily stem from weak fundamentals. A fundamentally weak asset—a less-than-stellar company’s stock, a speculative-grade bond or a building in the wrong part of town—can make for a very successful investment if bought at a low-enough price.

Making Predictions

Second level thinking has nothing to do with making predictions about future. Future is inherently unknown, and second level thinking recognizes that.

Second level thinking emphasizes the importance of going beyond surface-level analysis and warns us against acting like prophets. Making prophecies does not make us second-level thinkers.

Most of the investors I’ve met over the years have belonged to the “I know” school. It’s easy to identify them.

• They think knowledge of the future direction of economies, interest rates, markets and widely followed mainstream stocks is essential for investment success.

• They’re confident it can be achieved.

• They know they can do it.

• They’re aware that lots of other people are trying to do it too, but they figure either (a) everyone can be successful at the same time, or (b) only a few can be, but they’re among them.

• They’re comfortable investing based on their opinions regarding the future.

• They’re also glad to share their views with others, even though correct forecasts should be of such great value that no one would give them away gratis.

• They rarely look back to rigorously assess their record as forecasters. Confident is the key word for describing members of this school.

We must be careful with overconfidence in our ability to predict the future.

On the contrary second level thinking embraces our lack of foresight.

For the “I don’t know” school, on the other hand, the word—especially when dealing with the macro-future—is guarded. Its adherents generally believe you can’t know the future; you don’t have to know the future; and the proper goal is to do the best possible job of investing in the absence of that knowledge.

…those who feel they don’t know what the future holds will act quite differently: diversifying, hedging, levering less (or not at all), emphasizing value today over growth tomorrow, staying high in the capital structure, and generally girding for a variety of possible outcomes.

This approach is unpopular. Quite often, hubris gets better of us, as we are driven by our need to get recognized and appreciated.

As a member of the “I know” school, you get to opine on the future (and maybe have people take notes). You may be sought out for your opinions and considered a desirable dinner guest . . . especially when the stock market’s going up. Join the “I don’t know” school and the results are more mixed. You’ll soon tire of saying “I don’t know” to friends and strangers alike. After a while, even relatives will stop asking where you think the market’s going. You’ll never get to enjoy that one-in-a-thousand moment when your forecast comes true and the Wall Street Journal runs your picture.

Understanding the Environment

Managing risk is all about knowing the future, but we cannot know the future unless we are prophets. The next best thing in absence of foresight is to know where you are. A key ingredient of knowing where you are is all about knowing the environment in which we operate.

The Importance of Market Cycles

Marks stresses that cycles are an inherent part of investing, and the biggest opportunities often come when people forget this fundamental truth. It’s easy to get caught up in the hype when the market’s soaring, but smart investors know that what goes up must come down.

Very few things move in a straight line. There’s progress and then there’s deterioration. Things go well for a while and then poorly. Progress may be swift and then slow down. Deterioration may creep up gradually and then turn climactic. But the underlying principle is that things will wax and wane, grow and decline.

Avoiding Psychological Traps

It is important to think critically about market trends and avoid common psychological traps of recency bias and herd mentality.

Ignoring cycles and extrapolating trends is one of the most dangerous things an investor can do. People often act as if companies that are doing well will do well forever, and investments that are outperforming will outperform forever, and vice versa. Instead, it’s the opposite that’s more likely to be true. The first time rookie investors see this phenomenon occur, it’s understandable that they might accept that something that’s never happened before—the cessation of cycles—could happen. But the second time or the third time, those investors, now experienced, should realize it’s never going to happen, and turn that realization to their advantage.

Resisting the urge to extrapolate current trends is difficult but necessary in order to manage risk. To position yourself to navigate market ups and downs we must understand where we are.

The Credit Cycle

The credit cycle provides a good map of where we are:

The longer I’m involved in investing, the more impressed I am by the power of the credit cycle. It takes only a small fluctuation in the economy to produce a large fluctuation in the availability of credit, with great impact on asset prices and back on the economy itself. The process is simple:

• The economy moves into a period of prosperity.

• Providers of capital thrive, increasing their capital base.

• Because bad news is scarce, the risks entailed in lending and investing seem to have shrunk.

• Risk averseness disappears.

• Financial institutions move to expand their businesses—that is, to provide more capital.

• They compete for market share by lowering demanded returns (e.g., cutting interest rates), lowering credit standards, providing more capital for a given transaction and easing covenants. At the extreme, providers of capital finance borrowers and projects that aren’t worthy of being financed. As The Economist said earlier this year, “the worst loans are made at the best of times.” This leads to capital destruction—that is, to investment of capital in projects where the cost of capital exceeds the return on capital, and eventually to cases where there is no return of capital. When this point is reached, the up-leg described above—the rising part of the cycle—is reversed.

• Losses cause lenders to become discouraged and shy away.

• Risk averseness rises, and along with it, interest rates, credit restrictions and covenant requirements.

• Less capital is made available—and at the trough of the cycle, only to the most qualified of borrowers, if anyone.

• Companies become starved for capital. Borrowers are unable to roll over their debts, leading to defaults and bankruptcies.

• This process contributes to and reinforces the economic contraction.

Of course, at the extreme the process is ready to be reversed again. Because the competition to make loans or investments is low, high returns can be demanded along with high creditworthiness. Contrarians who commit capital at this point have a shot at high returns, and those tempting potential returns begin to draw in capital. In this way, a recovery begins to be fueled. I stated earlier that cycles are self-correcting. The credit cycle corrects itself through the processes described above, and it represents one of the factors driving the fluctuations of the economic cycle. Prosperity brings expanded lending, which leads to unwise lending, which produces large losses, which makes lenders stop lending, which ends prosperity, and on and on.

Knowing what’s happening around us is the key.

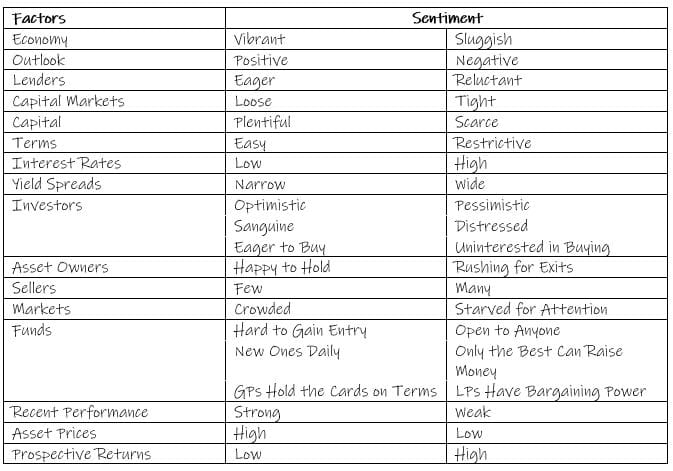

Market Psychology and Sentiment

Understanding where we are requires us to understand market psychology at various times.

Once in a while we experience periods when everything goes well and riskier investments deliver the higher returns they seem to promise. Those halcyon periods lull people into believing that to get higher returns, all they have to do is make riskier investments. But they ignore something that is easily forgotten in good times: this can’t be true, because if riskier investments could be counted on to produce higher returns, they wouldn’t be riskier.

During bull markets, when everything seems to be going up, it’s easy to fall into the trap of thinking that the best way to boost your returns is to take on more risk. After all, if speculative, high-risk investments are delivering great results, why not jump on the bandwagon?

…be alert to what’s going on around you with regard to the supply/demand balance for investable funds and the eagerness to spend them.

But this way of thinking ignores a fundamental truth about risk: if risky investments could be counted on to always deliver higher returns, then they wouldn’t be risky. The whole reason they’re considered risky is because there’s a significant chance that they won’t pan out, leaving investors with losses instead of gains.

The risk-is-gone myth is one of the most dangerous sources of risk, and a major contributor to any bubble. At the extreme of the pendulum’s upswing, the belief that risk is low and that the investment in question is sure to produce profits intoxicates the herd and causes its members to forget caution, worry and fear of loss, and instead to obsess about the risk of missing opportunity.

Eventually the tide goes out, that is the natural order of things. As Warren Buffet says, “its only when the tide goes out that you find out who’s been swimming naked”.

Cycles are self-correcting, and their reversal is not necessarily dependent on exogenous events. They reverse (rather than going on forever) because trends create the reasons for their own reversal. Thus, I like to say success carries within itself the seeds of failure, and failure the seeds of success.

The key is to stay grounded and avoid getting swept up in the euphoria or despair of the moment.

Howard Marks presents the following checklist to get a pulse check on where we are:

If we see more checkmarks in the left-hand sentiment column, the level of risk is higher.

…skepticism and pessimism aren’t synonymous. Skepticism calls for pessimism when optimism is excessive. But it also calls for optimism when pessimism is excessive.

Margin of Safety

Marks advises investors to insist on a significant buffer between the price they pay for an asset and its intrinsic value. It’s like buying a house: you wouldn’t pay full price for a fixer-upper, would you? You’d want a discount to account for the work and risk involved. The same goes for investing: by buying assets at a steep discount, you give yourself a cushion against unexpected setbacks.

Building a buffer

Overreliance on expected outcomes can be dangerous.

“Never forget the six-foot-tall man who drowned crossing the stream that was five feet deep on average.”

While understanding average or expected outcomes is important, don’t build a strategy that only works under these conditions. You must plan for outliers.

Relying to excess on the fact that something “should happen” can kill you when it doesn’t. Even if you properly understand the underlying probability distribution, you can’t count on things happening as they’re supposed to. And the success of your investment actions shouldn’t be highly dependent on normal outcomes prevailing; instead, you must allow for outliers.

By acknowledging the limitations of our predictive abilities and the potential for outlier events, we can build resilience by making an allowance for losses.

The principle of maintaining buffers, or a margin of safety, can be applied to our personal and professional lives, particularly in how we build and maintain relationships. Just as financial buffers protect against unexpected losses in investing, emotional and psychological buffers can safeguard relationships during challenging times. These buffers can be built through building trust, open communication, show of appreciation, empathy, understanding and shared experiences.

Just as in investing, where a margin of safety helps portfolios weather market downturns, these emotional and psychological buffers in relationships can help you through stressful periods, conflicts, or external pressures without completely eroding the underlying trust and connection.

Ensuring Survival

Margin of safety is fundamentally about ensuring survival. In both investing and life, success typically unfolds over time, with overnight triumphs being rare exceptions. To achieve long-term success, one must first and foremost survive.

…an excellent investor may be one who—rather than reporting higher returns than others—achieves the same return but does so with less risk (or even achieves a slightly lower return with far less risk).

The true value of this strategy often remains hidden during stable or rising markets.

Of course, when markets are stable or rising, we don’t get to find out how much risk a portfolio entailed. That’s what’s behind Warren Buffett’s observation that other than when the tide goes out, we can’t tell which swimmers are clothed and which are naked. It’s an outstanding accomplishment to achieve the same return as the risk bearers and do so with less risk. But most of the time it’s a subtle, hidden accomplishment that can be appreciated only through sophisticated judgments.

In other words, the benefits of a prudent, risk-aware approach become apparent during market downturns. Achieving returns comparable to higher-risk strategies, but with lower risk, is a remarkable accomplishment.

Margin of safety principle reminds us that in investing, as in life, the race is not always to the swift, but to those who can stay in the race.

Circle of Competence

Just like you wouldn’t try to perform brain surgery without years of training and practice, you shouldn’t invest in markets or strategies you don’t fully understand. Sticking to what you know may limit your opportunities, but it also helps you avoid hidden risks and pitfalls.

Before trying to compete in the zero-sum world of investing, you must ask yourself whether you have good reason to expect to be in the top half. To outperform the average investor, you have to be able to outthink the consensus. Are you capable of doing so? What makes you think so?

It’s a tough question, but an important one. Do you have access to information or insights that others don’t? Do you have a proven track record of making smart investment decisions? Do you have the emotional discipline to stay the course when markets get rocky?

Competence in investing has a lot to do with managing emotions as opposed to knowing the technical aspects of financial markets.

In finance, the soft skills (how you behave) is typically more powerful than the hard, technical skills.

Our emotions, especially greed and envy push us to venture beyond our circle of competence in search of higher gains without understanding the associated risks.

“The Cat, the Tree, the Carrot and the Stick.” The cat is an investor, whose job it is to cope with the investment environment, of which the tree is part. The carrot—the incentive to accept increased risk—comes from the higher returns seemingly available from riskier investments. And the stick—the motivation to forsake safety—comes from the modest level of the prospective returns being offered on safer investments. The carrot lures the cat to higher branches—riskier strategies—in pursuit of its dinner (its targeted return), and the stick prods the cat up the tree, because it can’t get dinner while staying close to the ground. Together, the stick and the carrot can cause the cat to climb until it ultimately arrives high up in the tree, in a treacherous position. The critical observation is that the cat pursues high returns, even in a low-return environment, and bears the consequences—increased risk—although often unknowingly.

For us individual investors, Howard Marks’s metaphor offers valuable insights:

- Be aware of your position: Understand where you are on the risk spectrum (how high up the tree you’ve climbed).

- Recognize the forces at play: Be conscious of both the allure of high returns and the push from low yields on safer investments.

- Consider the downside: Remember that being high up in the tree means a longer, more dangerous fall.

- Avoid unconscious risk-taking: Regularly assess your risk exposure to avoid unknowingly climbing too high.

- Balance risk and return: Find a position in the tree that balances your need for returns with your risk tolerance.

Managing Emotions

Developing competence has a lot to do with recognizing and managing our emotions.

Greed

Greed is an extremely powerful force. It’s strong enough to overcome common sense, risk aversion, prudence, caution, logic, memory of painful past lessons, resolve, trepidation and all the other elements that might otherwise keep investors out of trouble. Instead, from time to time greed drives investors to throw in their lot with the crowd in pursuit of profit, and eventually they pay the price.

Acknowledging the power of greed and actively working to counteract its influence, you can make more rational, considered decisions. This can help avoid the pitfalls of bubble-like market conditions and contribute to more stable, sustainable long-term performance.

Fear

Fear, then, is more like panic. Fear is overdone concern that prevents investors from taking constructive action when they should.

The challenge of maintaining rational thought in stressful situations. Marks reminds us of our emotional reactions, while natural, can hinder rather than help us in achieving our goals.

Envy

…envy. However negative the force of greed might be, always spurring people to strive for more and more, the impact is even stronger when they compare themselves to others. This is one of the most harmful aspects of what we call human nature. People who might be perfectly happy with their lot in isolation become miserable when they see others do better. In the world of investing, most people find it terribly hard to sit by and watch while others make more money than they do.

Envy arises from comparing ourselves to others, rather than from absolute performance.

Recognizing the influence of envy and actively working to counteract its effects, you can make more rational decisions.

Ego

…ego. It can be enormously challenging to remain objective and calculating in the face of facts like these:

• Investment results are evaluated and compared in the short run.

• Incorrect, even imprudent, decisions to bear increased risk generally lead to the best returns in good times (and most times are good times).

• The best returns bring the greatest ego rewards.

When things go right, it’s fun to feel smart and have others agree. In contrast, thoughtful investors can toil in obscurity, achieving solid gains in the good years and losing less than others in the bad. They avoid sharing in the riskiest behavior because they’re so aware of how much they don’t know and because they have their egos in check.

We are programmed to seek immediate gratification and external validation. Managing our ego and resisting the allure of short-term validation are crucial skills for successful long-term investing.

Ultimately, staying humble is the key to being aware of one’s circle of competence and is the only way to broaden the circle.

Expanding the circle of competence

A key aspect of competence is understanding where your expertise ends, and uncertainty begins.

Investing in an unknowable future as an agnostic is a daunting prospect, but if foreknowledge is elusive, investing as if you know what’s coming is close to nuts. Maybe Mark Twain put it best: “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

By approaching investing with this humble, self-aware mindset, you can make more informed decisions within your areas of expertise while avoiding the pitfalls of venturing into unknown territory.

How do we expand our circle of competence and develop an edge?

The more we concentrate on smaller-picture things, the more it’s possible to gain a knowledge advantage. With hard work and skill, we can consistently know more than the next person about individual companies and securities, but that’s much less likely with regard to markets and economies. Thus, I suggest people try to “know the knowable.”

Mastery often comes from concentrating our efforts on specific areas sustained over a long period and avoid making predictions.

Who Should Read It?

So, who should read Howard Marks’s “The Most Important Thing”? Honestly, anyone can find value in it. Whether you’re an experienced investor, a curious beginner, or just someone looking to make smarter decisions, this book has practical insights for you.

For Investors: If you invest, this book is essential. Marks explains complex ideas in simple terms, helping you think critically, manage risk, and stay within your expertise. It’s not just about chasing returns; it’s about understanding the game and the environment. You’ll learn to spot hidden risks, think ahead, and avoid common mistakes.

For Non-Investors: Even if you’re not into finance, the principles apply to everyday life. Making a career move, starting a new relationship, or tackling a big project? The same rules apply. Knowing when to be cautious, when to take a chance, and how to balance risk and reward can make a big difference.

For Everyone: This book is for anyone who wants to make better decisions. Marks talks about humility, discipline, and patience – traits that are useful beyond investing. By knowing our limits and understanding our strengths, we can handle life’s uncertainties with more confidence.

So, whether you’re managing a portfolio, planning your next career step, or just trying to make smarter choices, “The Most Important Thing” offers practical wisdom. It’s about building a mindset that understands complexity, seeks clarity, and prepares for whatever comes next.

In short, if you want to think better and live smarter, this book is for you. Happy reading!