Show me how you measure me, and I’ll show you how I behave.

This fundamental truth about incentives runs through every business decision ever made. As Adam Smith observed in The Wealth of Nations, “It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest.” Like a river, incentives shape the flow, speed, and direction of human behavior—often in ways that aren’t immediately obvious to system designers.

The consequences can be surprising. When British colonial rulers in India offered bounties for dead cobras, they created cobra farming instead of cobra extinction. When the Italian Air Force in WWI allowed pilots to choose their targets, they repeatedly bombed the same defenseless area of Corfu. As Moses Maimonides understood centuries ago, human behavior follows a simple rule: people move towards what they find agreeable, and away from what they find disagreeable.

John Malone understood this relationship between measurement and behavior better than most. When he walked into TCI’s offices in 1973, he saw how traditional accounting metrics were creating exactly the wrong incentives for the cable industry. His solution would reshape not just his company, but modern business itself.

He found a capital-intensive business suffocating under conventional accounting metrics. The cable industry required massive upfront investments: laying cable infrastructure, upgrading equipment, and acquiring local franchises. Under standard accounting principles, these investments triggered large depreciation and amortization charges that devastated reported earnings, even when the underlying business was generating substantial cash flow.

The incentive problem was clear: If you measure a business solely by its reported earnings, you create a powerful disincentive to make the very investments needed for long-term success. Wall Street’s obsession with quarterly profits was effectively punishing companies for growing. As Malone would later tell investors:

“If you’re going to ask about quarterly earnings, you’re at the wrong meeting, and you probably own the wrong stock.”

The measurement system itself needed to change. Traditional metrics like net income included non-cash charges like depreciation and amortization, which didn’t reflect the actual cash-generating ability of cable assets. They also included interest expenses, which were more a reflection of financing decisions than operational performance. And taxes, while real costs, varied significantly based on depreciation schedules and debt levels.

Malone’s solution was EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. This metric stripped away the accounting noise to reveal a business’s underlying cash-generating potential. For TCI, it created a new incentive structure that aligned with long-term value creation rather than short-term profit reporting.

But like all incentive systems, EBITDA would have its own unintended consequences…

The Anatomy of EBITDA

To understand EBITDA’s power—and its dangers—we need to dissect its components. As Richard Hamming noted, “You get what you measure.” Each element of EBITDA was chosen with precise purpose:

Start with earnings—the basic profit a company generates from operations. Then add back:

- Interest: A financing decision, not an operational one

- Taxes: Which vary by jurisdiction and structure

- Depreciation and Amortization: Non-cash charges that account for asset wear and tear

The brilliance lay in what each add-back revealed about true business performance. But this was just the beginning. As businesses grew more complex, so did their adjustments to EBITDA. Companies began adding back “one-time” expenses, restructuring costs, and other items they deemed non-recurring. This “Adjusted EBITDA” offered even more flexibility—perhaps too much. As one wit observed, EBITDA became “earnings before anything bad happens.”

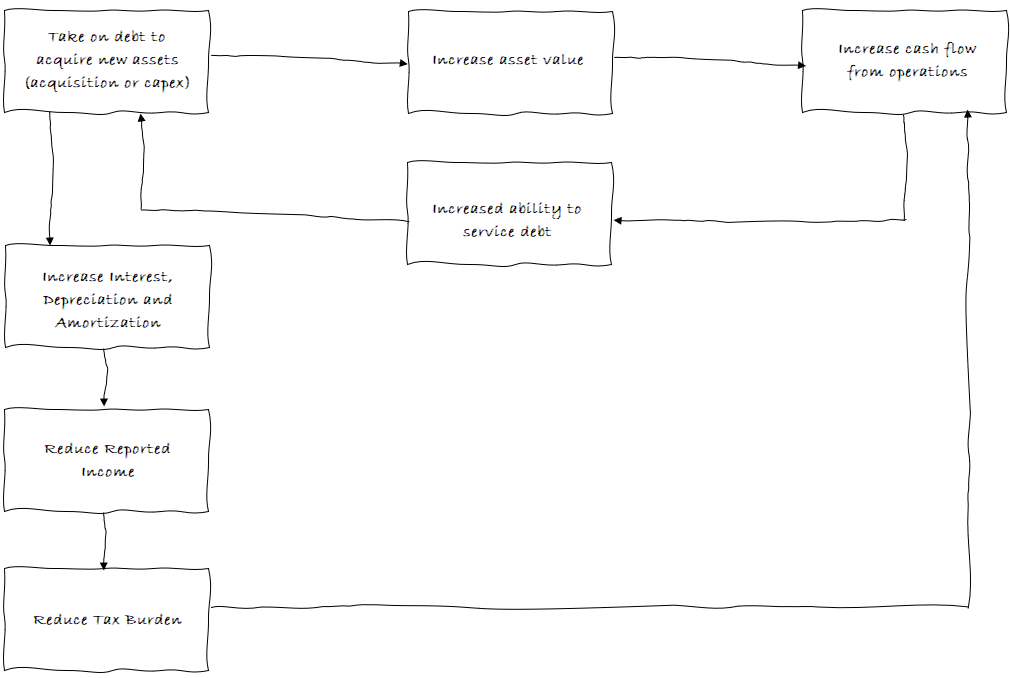

For TCI, even the basic EBITDA calculation revealed something crucial. Take a typical cable franchise acquisition: say TCI borrowed $10 million to buy a system generating $2 million in annual cash flow. Traditional earnings would show a loss due to interest payments ($800,000) and depreciation ($1 million). But EBITDA would show the true $2 million of cash-generating potential. Multiply this across hundreds of acquisitions, and you can see why Malone’s metric mattered.

This wasn’t just financial engineering—it was incentive engineering. As Howard Marks would later observe, “I’ve given up on getting them to do what I tell them to do; they do what I pay them to do.” EBITDA gave TCI’s managers permission to think bigger, to make investments that looked terrible on a GAAP earnings basis but created enormous long-term value. It aligned incentives with long-term value creation, giving Wall Street a new lens through which to view capital-intensive businesses.

The TCI Revolution

Armed with EBITDA, Malone executed one of the most aggressive growth strategies in business history. As Will Thorndike explains in The Outsiders:

“Malone [realized] that maximizing [reported] earnings… the holy grail for most public companies at that time, was inconsistent with the pursuit of scale in the nascent cable television industry. To Malone, higher net income meant higher taxes, and he believed that the best strategy for a cable company was to use all available tools to minimize reported earnings and taxes, and fund internal growth and acquisitions with cash flow…”

The strategy was beautifully simple: borrow money to buy cable franchises, use the cash flow from these acquisitions to pay down debt, and repeat. EBITDA made this possible by showing lenders and investors the true cash-generating potential of these assets, even when traditional earnings looked dismal.

This wasn’t just about financial metrics—it was about creating the right incentives throughout the organization. Malone was so committed to this approach that he famously threatened to fire any accountant who showed a profit. This wasn’t mere bravado—it was a clear signal about priorities. As Warren Buffett would later observe about institutional behavior, “My most surprising discovery: the overwhelming importance in business of an unseen force that we might call ’the institutional imperative.'”

The results were staggering. Over two decades, TCI delivered average annual returns of more than 30%. By the time Malone sold to AT&T in 1999, the company was worth around $50 billion. But perhaps more importantly, he had created a new way of thinking about business value—one that would spread far beyond the cable industry.

The Double-Edged Sword

Like the cobra effect in colonial India, EBITDA created its own set of unintended consequences. Not all EBITDA was created equal. While Malone used depreciation and amortization to shelter TCI’s genuine cash flows from taxes, others would use EBITDA to mask fundamentally weak businesses.

The metric’s popularity created new incentive problems. Companies began treating routine expenses as “extraordinary” items, excluding them from their EBITDA calculations. More insidiously, some businesses began aggressively capitalizing costs that should have been expensed. Since depreciation would be added back in EBITDA calculations, this accounting maneuver artificially inflated the metric. What Malone had designed as a tool for understanding capital-intensive businesses became, in some cases, a shield for poor performance.

The distortions were particularly acute in leveraged buyouts. In 2005, KKR, Bain Capital, and Vornado Realty Trust acquired Toys “R” Us in a $6.6 billion leveraged buyout, using an EBITDA multiple of 7.6x to justify the valuation. The deal loaded Toys “R” Us with $5.3 billion in debt, secured by its real estate assets. The company’s SEC filings show how EBITDA calculations excluded critical expenses like store maintenance capital expenditures and digital infrastructure investments—precisely the investments needed to compete with Amazon. By 2017, interest payments consumed nearly $425 million annually, while operating income was just $460 million.

Commercial real estate saw similar distortions. General Growth Properties, once America’s second-largest mall operator, used EBITDA-based metrics to justify taking on $27.3 billion in debt by 2008. The company’s SEC filings reveal how they excluded maintenance costs and treated declining tenant revenues as “temporary,” maintaining inflated EBITDA projections even as retail trends shifted permanently. The 2009 bankruptcy filing revealed the gap between EBITDA projections and actual cash available for debt service.

The broader commercial real estate market followed this pattern. From 2005 to 2007, Commercial Mortgage-Backed Securities (CMBS) were frequently priced using EBITDA multiples that assumed perpetual rent growth. When Lehman Brothers collapsed in 2008, their commercial real estate portfolio revealed how EBITDA-based valuations had systematically ignored both cyclical risks and structural changes in office space demand.

As Warren Buffett observed, “People who use EBITDA are either trying to con you or con themselves.” The metric that had originally helped TCI make sound long-term investments was now being used to rationalize unsustainable financial engineering.

This evolution was predictable. Just as measuring cobra kills led to cobra farming, measuring EBITDA led to EBITDA engineering. The very flexibility that made EBITDA useful in Malone’s hands made it dangerous in others'.

Modern Mutations

If Malone’s EBITDA was a simple tool to understand cash flows, its modern descendants are something else entirely — financial alchemy that would make medieval chemists proud.

The 2008 financial crisis opened Pandora’s box. Like a virus mutating to survive, EBITDA evolved. Companies didn’t just add back depreciation and amortization anymore; they began a sophisticated game of “adjustments.” Restructuring charges appeared with clockwork regularity yet somehow remained “non-recurring.” Acquisition costs were added back before deals even closed. Stock-based compensation vanished from calculations, as if paying employees in equity cost nothing at all.

But it was the tech sector that truly elevated EBITDA engineering to an art form:

- “Run-rate EBITDA”: Take your best month ever and pretend every month is just like it

- “Contribution margin EBITDA”: Ignore the cost of acquiring customers, because surely they’ll keep coming for free

- Platform-based adjustments: That billion-dollar infrastructure investment? Just a one-time thing, trust us

- “Adjusted EBITDA margins”: Using gross revenue instead of net, because bigger numbers look better

The SaaS industry pushed even further. R&D costs? That’s an investment—add it back. Hosting costs? Just scaling expenses—add those back too. Sales commissions? Capitalize them over an optimistically long customer lifetime. Each adjustment moved further from Malone’s original vision of understanding true cash generation.

Then came COVID-19, and with it, EBITDAC—Earnings Before Interest, Taxes, Depreciation, Amortization, and Coronavirus. Companies didn’t just add back direct pandemic costs; they calculated theoretical revenues they “would have earned” in a parallel, pandemic-free universe.

These mutations follow a predictable pattern:

- Identify anything that hurts GAAP earnings

- Label it “non-recurring” or “investment”

- Add it back to EBITDA

- Invent a new metric name to normalize for your industry’s unique “challenges”

What began as Malone’s flashlight to illuminate cash flows had become a fun-house mirror, distorting business reality beyond recognition. As one analyst quipped, “At this rate, we’re not far from EBITDAPLS—Earnings Before Interest, Taxes, Depreciation, Amortization, and Profit-Losing Segments.”

The Measurement Paradox

The story of EBITDA reveals a deeper truth about business metrics: they shape the very reality they attempt to measure. Malone understood this when he created EBITDA—he wasn’t just measuring TCI’s performance; he was creating incentives for long-term value creation.

But measurement systems have a way of escaping their creators’ intentions. As companies learned to engineer their EBITDA, the metric began driving behavior rather than illuminating it. CFOs spent more time crafting adjustments than improving operations. Boards approved acquisitions based on “adjusted” projections that bore little resemblance to reality. Investment bankers pitched deals using increasingly creative EBITDA multiples.

The evolution mirrors what Richard Hamming observed about measurement systems: “You get what you measure, and what you measure changes what you get.” EBITDA started as a tool for understanding cash flows in capital-intensive businesses. But like the cobra bounty system, it created incentives that changed behavior in ways its creator never intended.

Perhaps the most important lesson from EBITDA’s evolution is one about human nature itself. As Charlie Munger observed, “Never, ever, think about something else when you should be thinking about the power of incentives.” Malone’s genius wasn’t just in creating EBITDA—it was in understanding how it would shape behavior and using that understanding to build value.

Today’s investors face a more complex challenge. They must not only understand what EBITDA and its variants measure, but also how these metrics influence management behavior. In a world of adjusted, modified, and normalized earnings, Malone’s original insight remains more relevant than ever: the difference between creating wealth and reporting income is all about incentives.