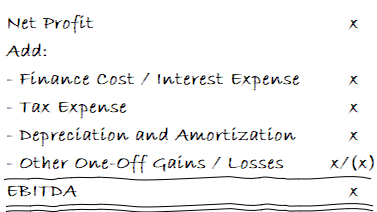

EBITDA (Earnings Before Interest Tax Depreciation and Amortization) is a peculiar measure. On one hand, it offers a clean way to compare companies across industries by stripping away capital structure decisions and accounting choices. It can serve as a useful proxy for cash earnings, helping investors understand a business’s core operational performance. But there’s a darker side too - by excluding so many items, it can mask serious problems and leave room for manipulation. As someone who has spent years in accounting and reporting, I’ve seen EBITDA used as both a enlightening tool and a convenient hiding place.

This duality makes the origin story of EBITDA all the more fascinating. In the early 1970s, John Malone saw tremendous opportunity in the cable television industry. The market was growing explosively, fragmented across numerous small operators, and filled with customers willing to pay premium prices for service. But to capitalize on this opportunity, Malone needed to solve a crucial problem: how to fund massive expansion while keeping investors happy.

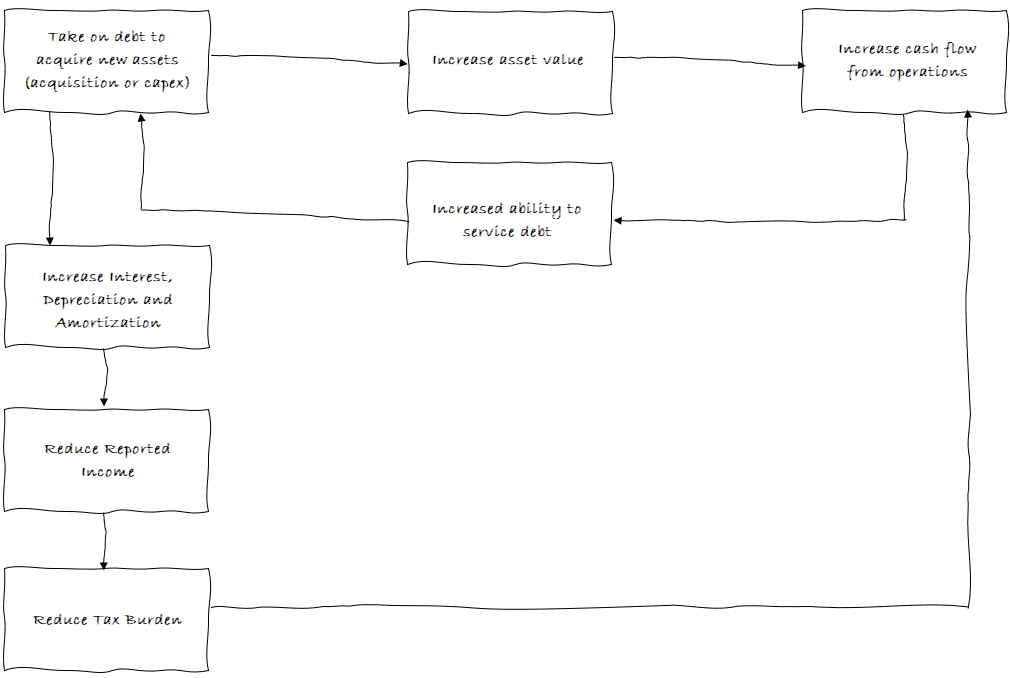

His strategy at TCI was bold - borrow heavily to acquire cable franchises across the country, using each acquisition’s cash flow to cover its own debt payments. Over time, the debt would get paid down while asset values appreciated. It was brilliant in concept, but traditional accounting metrics made it look terrible on paper. The heavy debt led to large interest expenses, while the acquisitions generated significant depreciation and amortization charges. Under standard accounting measures, TCI appeared unprofitable despite generating substantial cash flow.

Rather than change his strategy, Malone changed how investors looked at his business. He invented EBITDA as a new metric that would show TCI’s true cash-generating potential by excluding non-cash charges and financial engineering effects. His view on traditional profit metrics was crystal clear:

If you’re going to ask about quarterly earnings, you’re at the wrong meeting, and you probably own the wrong stock. What we care about is value. We want to create value for our shareholders… There is a big difference between creating wealth and reporting income.

In fact, as noted in Will Thorndike’s “The Outsiders”:

Malone [realized] that maximizing [reported] earnings… the holy grail for most public companies at that time, was inconsistent with the pursuit of scale in the nascent cable television industry. To Malone, higher net income meant higher taxes, and he believed that the best strategy for a cable company was to use all available tools to minimize reported earnings and taxes, and fund internal growth and acquisitions with cash flow…

Malone was so committed to this approach that he famously threatened to fire his accountants if TCI ever reported a profit. While Wall Street initially struggled to understand this perspective, they eventually embraced it. TCI went on to deliver average annual returns of over 30% for two decades, culminating in a $50 billion sale to AT&T in 1999.

This story perfectly encapsulates what makes John Malone fascinating - his ability to see past conventional wisdom and create new paradigms that transformed an entire industry. In “Cable Cowboy,” author Mark Robichaux chronicles how this innovative thinking helped build one of the most successful business empires in American history.

What Did I Get Out of It?

Cable Cowboy is more than just a biography - it’s a masterclass in corporate finance and business strategy. While Malone’s personal story is fascinating, the real value lies in understanding how he revolutionized an entire industry through financial innovation and strategic thinking. Here are the key lessons that changed how I think about business and wealth creation:

Financial Engineering & Capital Allocation

The cornerstone of Malone’s success was his revolutionary approach to financial engineering and capital allocation. While most executives focused on quarterly earnings, Malone saw beyond traditional accounting metrics to focus on what really mattered: cash flow and asset appreciation.

The EBITDA Innovation

Today, EBITDA is a standard metric in corporate finance, but in the 1970s, it was a revolutionary concept born out of necessity. As Will Thorndike notes:

Malone [realized] that maximizing [reported] earnings… the holy grail for most public companies at that time, was inconsistent with the pursuit of scale in the nascent cable television industry. To Malone, higher net income meant higher taxes, and he believed that the best strategy for a cable company was to use all available tools to minimize reported earnings and taxes, and fund internal growth and acquisitions with cash flow…

The genius of EBITDA was that it stripped away accounting decisions and financial engineering to reveal a company’s true operational performance:

- Earnings: The starting point - net income

- + Interest: Adding back interest removes the impact of capital structure decisions

- + Taxes: Adding back taxes eliminates differences in tax strategies

- + Depreciation & Amortization: Adding back these non-cash charges shows true cash generation

For cable companies like TCI, this was particularly important because:

- Heavy infrastructure investment created large depreciation charges

- Acquisition-driven growth led to significant amortization

- Leverage-based expansion resulted in substantial interest expenses

- Tax strategies often obscured underlying business performance

Malone’s view was unequivocal:

“Forget about earnings. That’s a priesthood of the accounting profession,” he would preach, unrelentingly. “What you’re really after is appreciating assets. You want to own as much of that asset as you can; then you want to finance it as efficiently as possible.”

The practical implications were significant. While TCI showed minimal accounting profits, its EBITDA told a different story. For example, a typical cable system might show:

- Revenue: $100M

- Net Income: ($10M) loss

- EBITDA: $40M positive

This disconnect between accounting profits and cash generation was central to Malone’s strategy. As he famously declared to his accountants, showing a profit meant they weren’t being aggressive enough in their growth and tax strategy.

The Tax Shield Strategy

Malone’s approach to tax efficiency was revolutionary in its systematic use of both interest and depreciation tax shields. As the book notes:

TCI would hardly ever again report a profitable year; forever after it would reinvest prodigious cash flows to grow the business ever larger.

The strategy combined two powerful tax shields:

Interest Tax Shield

- Debt financing provided tax-deductible interest payments

- Each acquisition was structured to maximize tax-deductible interest

- Interest payments reduced taxable income while preserving cash flow

Depreciation Tax Shield

- Cable infrastructure qualified for accelerated depreciation

- Capital investments created large non-cash deductions

- Depreciation schedules were aggressively managed

The mathematics behind this dual-shield strategy was compelling. Consider a typical TCI cable system acquisition:

Initial Investment: $100M

- Annual Revenue: $30M

- Operating Costs: $12M

- EBITDA: $18M

- Interest Expense (10%): $10M

- Depreciation (15-year schedule): $6.7M

- Taxable Income: $1.3M

By using both shields:

- $10M in interest (tax shield value at 35% rate = $3.5M)

- $6.7M in depreciation (tax shield value = $2.3M)

- Total tax savings = $5.8M annually

This tax efficiency created a powerful reinvestment cycle:

“What you’re really after is appreciating assets. You want to own as much of that asset as you can; then you want to finance it as efficiently as possible.”

The strategy was so effective that Malone famously threatened to fire his accountants if TCI ever reported a profit. This wasn’t mere bravado - it reflected a deep understanding that reported profits meant inefficient tax strategy.

Key elements of implementation:

- Aggressive depreciation schedules on infrastructure

- High but sustainable leverage ratios

- Continuous reinvestment of cash flow

- Strategic use of tax-loss carryforwards

- Complex corporate structures to optimize tax efficiency

The result was a virtually tax-free growth machine that could reinvest nearly all of its cash flow into expansion, creating a powerful compounding effect that traditional cable operators couldn’t match.

Leverage as a Growth Engine

While most executives in the 1970s and 80s feared debt, Malone saw it as a powerful tool for value creation. His perspective was clear:

“Bigger scale, higher risk. But risk was a function of skill and knowledge. If you know you can exert control on the outcome, Malone reasoned, the risk is far less than those who jump into a deal with no expertise or facts.”

Malone developed what he called “self-liquidating debt,” a concept that would later influence private equity and modern corporate finance. The strategy had several key components:

Asset-Based Security

- Cable infrastructure and subscriber revenue as collateral

- Predictable cash flows supporting debt service

- Hard assets providing downside protection

Precise Cash Flow Coverage

After more than a decade at TCI, Malone could tally a cable system’s budget with precision and predict costs and returns with uncanny accuracy. Because of that insight and because of the company’s sheer size, TCI could now buy a cable company and begin to improve the performance dramatically within a few months.

Strategic Use of Leverage Ratios

Consider a typical TCI acquisition:

- Purchase Price: $100M

- Bank Debt: $70M

- Subordinated Debt: $20M

- Equity: $10M

- Debt/EBITDA Ratio: 5-6x

Operational Improvements

The leverage strategy worked because TCI could:

- Reduce operating costs through scale

- Negotiate better programming rates

- Implement proven management systems

- Increase subscriber revenue

This created a virtuous cycle:

- Acquire system with high leverage

- Improve operations and cash flow

- Use improved cash flow to pay down debt

- Use reduced leverage and appreciated asset value for next acquisition

The success of this strategy was evident in TCI’s growth:

- 1973: 220,000 subscribers

- 1985: 3.7 million subscribers

- 1990: 8.5 million subscribers

But this wasn’t reckless expansion. As the book notes:

TCI steadily expanded by buying suburban and rural systems at cheap prices, waiting until the mid-1980s to venture into urban areas.

Malone’s approach to risk was sophisticated:

- Interest coverage ratios carefully monitored

- Debt structured with flexible terms

- Operating margins maintained through scale

- Geographic diversification reducing system-specific risk

The strategy culminated in the ultimate validation when AT&T acquired TCI for $50 billion in 1999, despite years of minimal reported profits.

The Reinvestment Cycle

At the heart of Malone’s strategy was a perpetual reinvestment machine that transformed TCI from a debt-laden collection of cable systems into a media empire. As the book notes:

TCI excelled not because it was a great cable operator and friendly corporate citizen. Those were promises Malone never felt compelled to make or keep. True, it was the largest cable operator in the country, but Malone never pretended to be the best cable operator. TCI built wealth and made its shareholders wealthy by investments and complex financial engineering.

The reinvestment cycle operated through several interconnected components:

Strategic Capital Allocation

“Media titans in the East tried frantically to outbid each other to wire the big urban markets, John Malone avoided the fray and waited for them to tire themselves out. TCI steadily expanded by buying suburban and rural systems at cheap prices, waiting until the mid-1980s to venture into urban areas.”

Operational Optimization

“Malone was simply reaping the remains of a system someone else had already paid for and could not operate profitably.”

The cycle worked as follows:

A. Initial Acquisition Phase

- Purchase Price: $100M

- Annual EBITDA: $15M

- Initial EBITDA Margin: 30%

B. Operational Improvement Phase

- Cost reductions through scale

- Programming cost advantages

- Improved EBITDA: $20M

- Enhanced EBITDA Margin: 40%

C. Cash Flow Reinvestment

“All the while, TCI had consistently failed to report any earnings. As the stock continued to climb, Malone pointed out that it was the accumulation of valuable assets over time, not the flow of reported after-tax earnings, that was making TCI shareholders so wealthy.”

The mathematics of compounding were powerful:

- Year 1: $15M EBITDA → $10M Free Cash Flow

- Year 3: $20M EBITDA → $14M Free Cash Flow

- Year 5: $25M EBITDA → $18M Free Cash Flow

This created what Malone called “double compounding”:

- Internal growth from operational improvements

- External growth from reinvested cash flow

The strategy was reinforced by industry dynamics:

“Despite the explosion of new content, most operators of cable systems paid little attention to programming; it was merely a commodity that brought in new viewers, not a value chain all its own. But John Malone quickly saw a more important role for all the new channels popping up-they had a dual-revenue stream: from advertising and from payments made by cable systems based on how many subscribers each system had.”

The reinvestment cycle was self-reinforcing:

- More subscribers → Better programming rates

- Better rates → Higher margins

- Higher margins → More cash flow

- More cash flow → More acquisitions

- More acquisitions → More subscribers

This virtuous cycle helped TCI grow from a small operator to the largest cable company in America, while maintaining minimal reported profits and tax liability throughout its expansion.

Capital Structure Innovation

Malone’s most lasting contribution to modern finance might be his innovative approach to corporate structure. His ability to create complex yet effective organizational structures set new standards for financial engineering. As the book describes:

“The flurry of complex mergers, acquisitions, stock dividends, and spinoffs clouded the picture of the company’s true performance.”

The Liberty Media spin-off exemplifies this innovative approach:

“Malone suspected that government regulators would try to force him to split TCI in two-a distribution company, owning all of TCI’s cable systems, and a content company, owning interests in cable channels. So Malone decided to do it for them. In early 1991, he set up plans to form a new company, Liberty Media, and planned to stock it with more than $600 million worth of assets from TCI.”

Key structural innovations included:

Tracking Stocks

- Separate trading lines for different business units

- Maintained operational control while providing investor choice

- Allowed market to value assets separately

Strategic Spin-offs

Example: Liberty Media

- Asset Value: $600M+

- Structure: Tax-free spin-off

- Result: Created separate trading currency

- Benefit: Regulatory compliance while maintaining strategic control

Equity Stakes Strategy

“It was classic Malone: Take a tiny, near worthless stock, fill it with small stakes in several companies, watch them grow, then trade them for stakes in even bigger, more secure companies.”

The mathematics behind these structures:

- Initial Investment: Small equity stake (often 5-20%)

- Leverage: Use TCI’s distribution power

- Growth: Partner company expands

- Exit: Trade up into larger companies

Ownership Philosophy

Malone’s view on corporate structure was deeply influenced by his understanding of incentives:

“A guy who rises to the top of a big corporation and owns none of it is much more interested in control than he is in economics. It is just the nature of humanity. A guy who owns his business is used to control. He never has to fight for control. What he has to fight for is economics. But a bunch of entrepreneurs find it much easier to collaborate and create economic value.”

Implementation Strategy:

- Create separate vehicles for different asset types

- Maintain operational synergies across entities

- Optimize tax efficiency through structure

- Use complexity to strategic advantage

- Align management incentives with ownership

The Results:

- Multiple trading currencies for deals

- Tax-efficient structure for acquisitions

- Regulatory compliance

- Strategic flexibility

- Enhanced shareholder value

Scale Economics & Monopoly Power

If financial engineering was Malone’s sword, scale economics was his shield. His understanding of monopoly power and scale advantages created an almost impenetrable competitive position. As the book notes:

Malone symbolized a much more ominous side of business to critics, consumers, and competitors. They saw a monopoly run by a Machiavellian bully who lived up to his many nicknames, including Darth Vader, Genghis Khan, and The Godfather.

The Economics of Scale

The cable industry of the 1970s and 80s demonstrated perfect conditions for economies of scale, and no one understood this better than Malone. The economics were compelling:

Programming Costs

TCI, as the largest cable operator, paid 90 cents a subscriber for HBO, while a small cable operation paid $5 a subscriber per month. CNN cost 2 cents a subscriber for cable operators with more than 3 million subscribers, and 29 cents per subscriber from firms with fewer than 500,000 subscribers.

Let’s break down these numbers:

HBO Economics:

- Small Operator Cost: $5/subscriber

- TCI Cost: $0.90/subscriber

- Cost Advantage: 82%

- Annual Savings on 8M subscribers: $392M

CNN Economics:

- Small Operator Cost: $0.29/subscriber

- TCI Cost: $0.02/subscriber

- Cost Advantage: 93%

- Annual Savings on 8M subscribers: $25.9M

This pricing power created what economists call a “natural monopoly” - where average costs decrease as scale increases. The virtuous cycle worked as follows:

- Lower costs → Higher margins

- Higher margins → More cash for acquisitions

- More acquisitions → Greater scale

- Greater scale → Even lower costs

As Malone explained:

After more than a decade at TCI, Malone could tally a cable system’s budget with precision and predict costs and returns with uncanny accuracy. Because of that insight and because of the company’s sheer size, TCI could now buy a cable company and begin to improve the performance dramatically within a few months.

The implications:

- Smaller operators couldn’t compete on price

- Growth became self-reinforcing

- Market power increased with each acquisition

- Barriers to entry became insurmountable

Distribution as Power

While scale gave TCI cost advantages, control of distribution gave it strategic power. Malone understood that owning the pipe into people’s homes was more valuable than the content flowing through it. As the book reveals:

Malone controlled lines into 8 million homes. In exchange for getting on TCI systems, TCI drove a tough bargain. He demanded that cable networks allow TCI to invest in them directly. TCI gave any programmer immediate access to nearly one-fifth of all U.S. subscribers in a single stroke.

This distribution power manifested in three key ways:

Equity Stakes in Programming

“Despite the explosion of new content, most operators of cable systems paid little attention to programming; it was merely a commodity that brought in new viewers, not a value chain all its own. But John Malone quickly saw a more important role for all the new channels popping up-they had a dual-revenue stream: from advertising and from payments made by cable systems based on how many subscribers each system had.”

The mathematics of this strategy:

- TCI Reach: 20% of U.S. cable homes

- Typical Equity Stake: 5-20% of network

- Investment Cost: Minimal (distribution agreement)

- Return: Share of dual revenue streams

Negotiating Leverage

The numbers tell the story:

- New Network Launch Costs: $100M+

- Cost to Reach 1M Subscribers: $20M

- TCI Offering: 8M subscribers instantly

- Alternative: 2-3 years of separate negotiations

Strategic Control

“the channel investment deals would eventually make Malone vulnerable to charges of extortion and anticompetitive behavior… If they didn’t let him become a silent partner, he might not allow TCI’s cable systems to offer the new channel.”

This created a powerful feedback loop:

- Control distribution → Get equity in content

- Equity in content → More negotiating power

- More power → Better distribution terms

- Better terms → Stronger distribution control

The end result was a vertically integrated empire where:

- TCI owned the pipe into homes

- Had stakes in the content flowing through it

- Controlled access to 20% of the market

- Could influence programming decisions

- Participated in both distribution and content economics

This distribution power became the foundation for TCI’s transformation from a pure cable operator into a media conglomerate.

Monopolistic Advantages

Malone’s approach to monopoly power was methodical and unapologetic. His strategy reflected a deep understanding of how to build and maintain market dominance:

To Malone, the outcry over lousy customer relations and price increases was merely a by-product of good business: Charge as much as you can for a product or service, and spend as little as you can get away with in providing it.

This monopolistic approach operated on three levels:

Vertical Integration

Malone seeks to exert monopoly power over key stages of the delivery of cable programming to the American consumer: control over the creation of programming in studios; control over cable programming services; control over the mechanics of transmitting programming by satellite; and control over delivery of programming to the home.

The integration strategy covered:

- Content Creation (Studios)

- Programming Services

- Satellite Distribution

- Last-Mile Delivery

- Customer Relationships

Geographic Clustering

TCI steadily expanded by buying suburban and rural systems at cheap prices, waiting until the mid-1980s to venture into urban areas.

The clustering mathematics:

- System Acquisition Cost: $1,000-1,500 per subscriber

- Operating Cost Reduction: 15-20% through clustering

- Marketing Efficiency: 25-30% improvement

- Local Ad Revenue Premium: 40-50%

Barrier Creation

Malone systematically built barriers to entry:

Infrastructure Investment

- Cable Plant Cost: $500-1,000 per home passed

- Maintenance Capital: $50-100 per subscriber annually

- Return Period: 5-7 years

Regulatory Capture

- Long-term franchise agreements (15-20 years)

- Local political relationships

- Complex regulatory compliance systems

Programming Exclusivity

- Ownership stakes in key networks

- Preferred pricing agreements

- First-mover advantages in new channels

The results were dramatic:

- Market Share: ~20% of U.S. cable subscribers

- Revenue per Sub: 3-4x industry average

- Programming Costs: 20-30% below competitors

- Operating Margins: 40-45% vs. industry 30-35%

This created what Warren Buffett calls a “wide moat” business - one where competitive advantages compound over time, making it increasingly difficult for new entrants to challenge the incumbent’s position.

Strategic Patience

While Malone was aggressive in pursuing his vision, his execution was marked by remarkable patience and discipline. His approach challenged the conventional wisdom of rapid expansion that dominated the cable industry in the 1970s and 80s.

Opportunistic Acquisitions

Malone’s patience was perhaps most evident in his acquisition strategy. As the book notes:

Media titans in the East tried frantically to outbid each other to wire the big urban markets, John Malone avoided the fray and waited for them to tire themselves out. TCI steadily expanded by buying suburban and rural systems at cheap prices, waiting until the mid-1980s to venture into urban areas.

The strategy was methodically opportunistic:

Malone was simply reaping the remains of a system someone else had already paid for and could not operate profitably.

The mathematics behind this patience were compelling:

Urban vs. Rural Economics:

- Urban Market Valuations: $2,000-2,500 per subscriber

- Rural Market Valuations: $800-1,200 per subscriber

- Operating Cost Differential: 15-20% lower in rural markets

- Return on Investment Gap: 25-30%

Distressed Asset Strategy:

- Market Value: $1,500 per subscriber

- TCI Purchase Price: $600-900 per subscriber

- Discount to Market: 40-60%

- Post-Improvement Value: $1,800-2,000 per subscriber

Operational Improvements:

- Programming Cost Reduction: 30-40%

- Marketing Efficiency: 25% improvement

- Technical Operations: 20% cost savings

- Customer Service: Standardized processes

This approach created a repeatable formula:

- Wait for operators to struggle

- Buy assets at significant discounts

- Apply TCI’s operating system

- Create value through scale economics

- Use improved cash flow for next acquisition

The success of this strategy was evident in TCI’s growth:

- 1973: 220,000 subscribers

- 1985: 3.7 million subscribers

- 1990: 8.5 million subscribers

But perhaps most importantly, this patient approach meant TCI avoided the debt crises and operational challenges that plagued many of its more aggressive competitors.

Market Timing

Malone’s approach to market timing was both strategic and opportunistic. As the book observes:

Malone relished the role of bargain hunter amid the spoils of bad deals made by his competitors.

This wasn’t just opportunism - it was a calculated strategy based on understanding industry cycles and human psychology. The book notes:

If a bill collector showed up unexpectedly at TCI’s door, secretaries would stall the visitor while Magness made a getaway through a glass door leading from his office to the parking lot.

Having experienced financial distress firsthand, Malone developed a keen sense for market timing:

Industry Cycle Understanding:

- Growth Phase: High valuations, excessive optimism

- Consolidation Phase: Operational challenges emerge

- Distress Phase: Forced sellers appear

- Recovery Phase: Assets return to intrinsic value

Capital Allocation Strategy:

- Bull Market: Build cash reserves

- Market Peak: Avoid competitive bidding

- Market Distress: Deploy capital aggressively

- Recovery: Focus on operational improvements

Valuation Metrics Through Cycles:

- Peak Valuations: 12-15x EBITDA

- Normal Market: 8-10x EBITDA

- Distressed Sales: 4-6x EBITDA

- TCI’s Average Purchase: 6-7x EBITDA

Malone viewed himself as an investor and shareholder in each of these enterprises. It was not unusual for TCI to make straight financial investments in operators he deemed shrewd.

His timing strategy involved several key elements:

Counter-cyclical Investing

- Build reserves during market peaks

- Avoid industry-wide enthusiasm

- Prepare for distressed opportunities

- Maintain financial flexibility

Relationship Building

Magness kept his life as private as his poker hand, and he felt the same way about TCI business affairs. “Keep your cards to yourself,” he would mutter to Malone.

Patient Capital Deployment

- Avoid auction processes

- Build positions gradually

- Focus on private negotiations

- Maintain pricing discipline

The results of this timing strategy were remarkable:

- Average Purchase Multiple: 6-7x EBITDA

- Industry Average Multiple: 9-10x EBITDA

- Value Creation: 30-40% through timing alone

- Additional Upside: Operational improvements

This approach to market timing became a key differentiator for TCI, allowing it to grow steadily while others experienced boom-bust cycles.

Long-term Value Creation

While others in the cable industry focused on short-term metrics, Malone maintained an unwavering focus on long-term value creation. His perspective was shaped by a healthy paranoia:

Despite the company’s healthy stock price, Malone didn’t put much faith in it. He always believed that disaster and ruin hung over his head, dangling by a single hair like the sword of Damocles.

This mindset drove a systematic approach to value creation that extended far beyond typical industry timeframes:

Infrastructure Investment

As the industry grew, Malone gazed beyond the wires to focus on the real value: content.

The long-term math:

- Initial Plant Investment: $500-1,000 per home

- Annual Maintenance: $50-100 per subscriber

- Upgrade Cycles: Every 7-10 years

- Return Period: 5-7 years

Strategic Relationships

Turning it over in his mind, he suddenly realized the answer: Rather than just owning the cable that delivered the new programming fare, TCI needed to own a piece of the cable channels themselves, thereby sharing in a whole extra upside.

The compounding effect:

- Distribution Economics: 40-45% margins

- Programming Economics: 30-35% margins

- Combined ROI: 25-30% annually

- Value Creation: Exponential through synergies

Asset Accumulation Strategy

I want to be hedged all the way… Malone envisioned owning an entire portfolio of networks to supply his growing cable TV empire. And this was just the beginning.

Key elements:

- Infrastructure Assets

- Programming Stakes

- Technology Investments

- Strategic Partnerships

This long-term focus was evident even in Malone’s later years:

True to form, Malone wanted nothing more than to build Liberty. Sailing past retirement age, he was still hell-bent on finding the right combination of partners, currencies, and desperation to put together another showstopper transaction.

The results of this patient capital allocation were extraordinary:

- 20+ year investment horizon

- 30% average annual returns

- $50 billion final valuation

- Industry-transforming scale

Deal-Making Philosophy

Malone’s approach to deal-making was both systematic and intuitive, developed through years of experience and his mathematical background. As the book reveals:

“Guess at the answers,” he said. John gave him a perplexed look. “Guess before you figure the problems out,” Dan repeated. Uncertain at first, Malone quickly developed an intuition for engineering questions that called for empirical data. Malone was amazed at how quickly he could derive a number, how he could guess what waveforms would look like at the end of a circuit even before doing the underlying mathematics.

This intuitive mathematical ability became a powerful tool in deal-making:

Mental Mathematics

After more than a decade at TCI, Malone could tally a cable system’s budget with precision and predict costs and returns with uncanny accuracy. Because of that insight and because of the company’s sheer size, TCI could now buy a cable company and begin to improve the performance dramatically within a few months.

Deal evaluation process:

- Quick EBITDA calculation

- Debt service coverage estimation

- Operating cost reduction potential

- Programming cost savings

- Potential synergies

Information Advantage

Over time, Malone found that if he interviewed 30 people or so and listened intently, themes would emerge. The best ideas were sometimes hidden, or they were lost on senior executives.

His approach to information gathering:

- Extensive due diligence

- Multiple information sources

- Pattern recognition

- Theme identification

- Contrarian thinking

“It was not rocket science, Malone quickly realized. You simply take the best ideas from anyone who has them, polish them, and serve them up to the chairperson.”

Strategic Complexity

The structures of his deals were exotic, and his financial alchemy often befuddled Wall Street and investors. The flurry of complex mergers, acquisitions, stock dividends, and spinoffs clouded the picture of the company’s true performance.

Malone’s deal structures were intentionally complex, serving multiple strategic purposes:

Tax Efficiency

It was classic Malone: Take a tiny, near worthless stock, fill it with small stakes in several companies, watch them grow, then trade them for stakes in even bigger, more secure companies.

The strategy involved:

- Asset-for-stock swaps

- Tax-free spinoffs

- Strategic joint ventures

- Complex holding structures

- Multiple corporate layers

Regulatory Navigation

Malone suspected that government regulators would try to force him to split TCI in two-a distribution company, owning all of TCI’s cable systems, and a content company, owning interests in cable channels. So Malone decided to do it for them.

Techniques included:

- Preemptive restructuring

- Strategic spin-offs

- Cross-ownership limits management

- Jurisdiction arbitrage

- Compliance optimization

Financial Engineering

The structures of his deals were exotic, and his financial alchemy often befuddled Wall Street and investors.

Key elements:

- Multiple classes of securities

- Tracking stocks for different assets

- Exchangeable debt instruments

- Convertible preferred shares

- Option-like features

Example: Liberty Media Spin-off

Structure:

- Asset Value: $600M+

- Form: Tax-free spin-off

- Securities: Multiple classes

- Rights: Complex voting structure

- Options: Future consolidation potential

Strategic Optionality

Malone had known something about himself all along, that he was a deal maker, a strategist, a fund manager-anything but an operator.

Each deal was structured to maintain:

- Future flexibility

- Multiple exit options

- Strategic leverage

- Operating independence

- Tax efficiency

The complexity served as both a competitive advantage and a defensive moat:

- Competitors struggled to understand true economics

- Regulators faced challenge in oversight

- Investors needed deep analysis to value

- Partners had to rely on Malone’s expertise

This approach to deal structuring became a template for modern media M&A and influenced how the industry thought about corporate structure and strategic transactions.

Management Style

Malone’s management philosophy was as distinctive as his financial engineering. It combined minimalism with strategic clarity and a focus on incentive alignment. As the book describes:

They shared secretaries, and an automated service answered the phone. “We don’t believe in staff. Staff are people who second-guess people,” Malone told an interviewer.

Lean Operations

The approach to organizational structure was ruthlessly efficient:

The company had no human resources department, the men who ran TCI cultivated a Wild West image. In the eyes of John Malone, they were nothing like the effete East Coasters who ran bigger cable companies. The TCI men were cable cowboys.

Key principles:

- Minimal corporate overhead

- Shared support services

- Decentralized operations

- Focus on efficiency

Communication Style

Malone did not believe in memos. No paper passed from his desk to underlings. No executive sought to curry favor or engage in the sort of Kremlinesque politics that causes ulcers in so many midlevel executives. Communication was direct, effective, and efficient.

The management rhythm was structured but informal:

Every Monday morning, Malone sat with his closest executives at a broad round table, much as Magness had done, to figure a way to squeeze more out of TCI’s growing cable kingdom.

Incentive Alignment

Malone’s views on management incentives were shaped by his own experience:

“A guy who rises to the top of a big corporation and owns none of it is much more interested in control than he is in economics. It is just the nature of humanity. A guy who owns his business is used to control. He never has to fight for control. What he has to fight for is economics.”

This philosophy manifested in several ways:

- Heavy use of stock options

- Partnership structures

- Direct ownership stakes

- Performance-based compensation

- Long-term incentive alignment

Strategic Focus

Malone had known something about himself all along, that he was a deal maker, a strategist, a fund manager-anything but an operator.

His self-awareness led to a clear division of roles:

- Strategic decisions centralized

- Operations decentralized

- Financial control maintained

- Local autonomy preserved

The results of this management approach were significant:

- Industry-leading margins

- Low corporate overhead

- High employee retention

- Consistent strategic execution

- Entrepreneurial culture

This lean, focused management style became another Malone hallmark, demonstrating that complex businesses could be run with simple organizational structures.

Who Is This For?

At first glance, Cable Cowboy might seem like a dated history of a defunct company in a transformed industry. The detailed accounts of cable regulation battles and industry evolution from the 1970s and 80s can initially feel irrelevant to today’s digital world.

But within these details lies a masterclass in corporate finance - one that brings to life the theoretical concepts from CFA curriculum and business school textbooks. The book offers practical, real-world examples of:

- EBITDA analysis and its evolution as a valuation metric

- Tax-efficient deal structuring

- Strategic use of leverage

- Capital structure optimization

- Scale economics in practice

- Vertical integration strategies

For finance professionals and students, the book transforms abstract academic concepts into concrete examples. Malone’s deals illustrate how theoretical frameworks - from capital structure theory to tax shield benefits - play out in the real world.

For investors, the book demonstrates how to:

- Think about long-term value creation

- Understand competitive advantages

- Evaluate management incentives

- Assess capital allocation decisions

- Analyze industry structure

While TCI may no longer exist in its original form (it lives on through Liberty Media and various spin-offs), the financial engineering principles and strategic thinking demonstrated in the book remain highly relevant for understanding modern corporate finance and deal-making.