Most people have been inside a house they don’t own but know intimately. You notice the creak in the hallway long before guests do. You know which window sticks in winter. You know where the light falls in the afternoon and which rooms cost more to heat than they should. Living in a place gives you a kind of knowledge that doesn’t show up on a floor plan.

Buying a house with a mortgage is built on that kind of familiarity. You put in a small amount of your own money, borrow the rest, and trust that the value of the house, and the life you build inside it, will be enough to justify the debt you’re taking on. The bank lends because the house is stable, the neighborhood is solid, and the risk feels contained.

A leveraged buyout isn’t very different in principle; it’s just amplified. A small group decides to “buy the house,” except the house is a multibillion-dollar company. They contribute a thin layer of their own equity. Everything else, sometimes ninety percent or more, comes from lenders willing to advance huge sums because the company throws off predictable cash. The buyers aren’t expected to carry the load themselves. The asset is expected to pay for its own purchase.

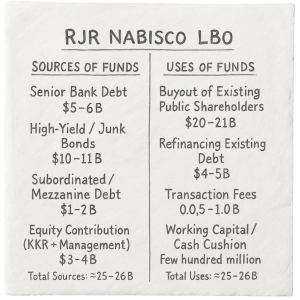

It starts with a document so plain it looks almost modest: a term sheet, two neat columns.

On the left, the sources of money: bank loans, bonds sold to investors, mezzanine lenders, and the sliver of equity the buyers themselves contribute.

On the right, the uses: what it costs to buy out the existing shareholders, the fees, the transaction expenses, the cash buffer required to keep operations steady.

Once the deal closes, the real shift happens quietly.

The company now bears the debt that was used to acquire it.

Pressure settles over everything. Costs get scrutinized. Business units are reconsidered. Assets that once seemed untouchable start to look negotiable. Every decision is filtered through the same question: does this help the company carry the weight now placed on its back?

And when the people leading that purchase are the same people who already run the company: people with complete access to its books, its vulnerabilities, and its hidden strengths, that’s a management buyout. The occupants decide to become the owners, using the house’s future income to finance the transaction.

Barbarians at the Gate is the story of what happens when this elegant, mortgage-like structure is stretched over one of America’s largest corporations. It shows how leverage magnifies ambition, how incentives warp judgment, and how a simple financing idea can swell into a bidding war that reshapes an entire company. Once you understand the mechanic: the buyers put in a little, borrow a lot, and rely on the company to shoulder the burden; the rest of the story becomes impossible to look away from.

What Did I Get Out of It

When you read Barbarians at the Gate, you realize leveraged buyouts aren’t really about finance, they’re about human nature, incentives, and information. While the big business story reads like a thriller; Barbarians at the Gate is a study in how people behave under big pressure, how decisions get made when the stakes are enormous. Here’s what stood out, with lessons that matter whether you’re running a company or just thinking about risk and reward.

Leverage is about access, not ownership

One of the strangest truths the book reveals is that you don’t actually need much money to buy a giant company, you just need to know how to pull the right levers. With an LBO, a handful of people with connections can control billions by borrowing against future cash flow. It flips the rules we think apply to everyday purchases completely upside down.

“You need money to be in this business. But not a lot. You need more money to open a shoe-shine shop than you do to buy a $2 billion company, let’s be honest about it.”

“But to buy a shoe-shine store, if it costs $3,000, you need $3,000. If you don’t got it in cash, you need to bring it by Thursday. But if it’s an LBO, not only do you not have to bring it, you don’t have to see it, you don’t know where you’re going to get it, nobody knows where they got it from. The whole situation comes from absolutely nothing.”

“This is a business for people who don’t have money, but who know somebody who has money, but who doesn’t put it up either…”

In some worlds, access and relationships can matter far more than resources on hand. The rules are different when you understand how to borrow against future potential. It’s a lesson in how the structures around us aren’t always what common sense would suggest, and how much power is shaped by who’s invited to the table, not just who shows up with a checkbook.

Incentives drive decisions

The engine behind nearly every big move in Barbarians at the Gate is simple: incentives. When executives see a chance to make “filthy rich” payouts from a buyout, priorities shift. Suddenly, the focus isn’t always on building a great company or serving shareholders; it’s on structuring deals that maximize personal gain, sometimes regardless of long-term consequences.

“On one thing they all agreed: The executives who launched LBOs got filthy rich.”

This scramble for upside comes at a cost. Critics see it as “stealing the company from its owners.” Budgets get slashed, research dries up, and everything gets sacrificed to service debt and reward the few at the top.

“Critics of this procedure called it stealing the company from its owners and fretted that the growing mountain of corporate debt…”

“Everyone knew LBOs meant deep cuts in research and every other imaginable budget, all sacrificed to pay off debt.”

While the argument is that debt forces efficiency; making companies “lean and mean”. What often happens is tunnel vision. Everything bends toward the incentive structure set by the deal. Incentives don’t just drive decisions, they warp them, redirecting energy and attention wherever the payoff is highest.

Debt brings discipline—and danger

LBOs force companies to become laser-focused on cash flow. With massive debt looming, every dollar gets scrutinized, and every part of the business is up for debate. Supporters argue that this pressure trims waste, leaving a “lean and mean” organization. But the reality is less tidy. When cutting costs is about survival, the axe often falls on more than just excess.

“Everyone knew LBOs meant deep cuts in research and every other imaginable budget, all sacrificed to pay off debt.”

Sometimes what gets cut isn’t fat, but muscle: things that support long-term health and innovation. The intense pressure to free up cash can erode the core of a business over time. And if projections are off by just a little, the consequences can be catastrophic; the margin for error is razor thin.

Debt can be a sharp tool for discipline, but it’s always two-edged. It might make a company more efficient, but it also makes it fragile. There’s no room for mistakes, and sometimes survival wins out over everything else.

Planning can be a mirage

One pattern you see over and over in the story is the gap between careful planning and what really happens. Elaborate reports, forecasts, and strategies make for good optics, but the reality is that the biggest moves, the ones that change everything, are driven by opportunity and instinct, not by sticking to the playbook.

“Nabisco executives prided themselves on the company’s elaborate planning procedures, compiled in thick, multiyear projections and operations outlooks.”

But as Johnson points out, real planning is much simpler, and often more about justifying action than delivering genuine insight.

“Planning, gentlemen, is ‘What are you going to do next year that’s different from what you did this year?’ he told them. ‘All I want is five items.’”

And when big change comes, it’s usually not because a committee mapped things out; it’s because someone sees an opening and goes for it.

“Recognize that ultimate success comes from opportunistic, bold moves which, by definition, cannot be planned.”

The takeaway: don’t fall for the comfort of process and paperwork. Most real outcomes are shaped by boldness and flexibility, not binders full of projections.

Control and information are everything

When it comes to leveraged buyouts, having control and access to inside information is the real edge. The insiders, the management team, hold the cards: they know the numbers, the hidden risks, and where the quick savings can be found. They can shape the deal and steer the outcome, while outsiders are left guessing.

“In an LBO, a small group of senior executives, usually working with a Wall Street partner, proposes to buy its company from public shareholders, using massive amounts of borrowed money.”

The battle for RJR Nabisco was shaped by who had the best data and could keep their plans secret the longest.

“The group with access to real numbers, confidential information, and who knows what to cut, wins.”

Kravis’s dilemma, as an outside bidder, was clear: he didn’t have the inside track.

“What if you’re Henry Kravis, and the fellows driving the car won’t even let you kick the tires?… In a bidding contest, Johnson and Cohen would hold all the cards. Not only did they have access to every piece of confidential information, they had a management team to analyze it.”

The process of due diligence: digging into every file, contract, and projection, is only possible if you have the trust and access that comes with being inside. That edge can define the winner in any high-stakes game, whether you’re buying a company or making a strategic move in your own career.

Process matters: for banks, for bids, for pride

The mechanics of high finance aren’t just about numbers, but also about rituals, status games, and perception. The details: who leads a bond offering, whose name goes “on the left” of a Wall Street tombstone ad, which firm gets top billing, become battles for position and ego as much as for deal terms. In Barbarians at the Gate, these seemingly minor distinctions shape outcomes, affect relationships, and sometimes even determine whether deals go through.

“The lead bank is so noted by placing its name first—on the left side—of the subsequent tombstone advertisements that pack The Wall Street Journal and other financial publications. Being ‘on the left’ of the tombstone thus has powerful symbolic significance in the bond world.”

At one point, the biggest takeover in history nearly collapsed because of a fight about who would get top billing on an ad.

“John Gutfreund and Tom Strauss were prepared to scrap the largest takeover of all time because their firm’s name would go on the right side, not the left side, of a tombstone advertisement buried among the stock tables…”

Process reveals what matters: sometimes it’s pride, not profit, that tips the scales. The story is a helpful reminder: watch for games within the game. When stakes are high, people fight for status as much as for money.

The human element warps outcomes

If there’s a constant in Barbarians at the Gate, it’s that big business isn’t just numbers: it’s people, with all their motives, egos, and blind spots. Board members approve golden parachutes to protect themselves. Executives set up legal trusts to guarantee their payouts, no matter who wins the bidding. Sometimes, the rational case for a decision gets lost in the fog of personalities, rivalries, and self-interest.

“The board also approved severance arrangements known as ‘golden parachutes’ for each of the company’s top ten officers. One thing puzzled staffers in the company’s treasury department. At Johnson’s direction, money for the parachutes was placed in protective trusts known as ‘rabbi trusts.’ Under the trusts’ terms, if RJR Nabisco changed hands, the new owner couldn’t touch these funds.”

There are moments when the game is played not for the company but for personal survival or status. Plans are made not just for the company’s good, but to ensure those at the top, no matter what happens, walk away winners.

The lesson is this: don’t assume incentives and rational analysis drive everything at the negotiating table. The human element: fear, self-preservation, reputation, and plain old spite, can shape outcomes just as much as money or logic.

The margin for error is razor thin

These deals aren’t built for mistakes. In an LBO, one wrong calculation, one optimistic projection, or one overlooked risk can collapse everything. The pressure to repay debt means there’s little slack. Minor missteps become major problems, and only relentless, precise due diligence separates success from disaster.

“His success depends on determining exactly how much debt the target company can take on, and figuring precisely what budgets can be cut and what businesses sold to pay down that debt quickly… His margin of error is so thin that a worn crank shaft or a blown gasket could prompt the bank to call his loan. Similarly, in an LBO, a wrong calculation or an inaccurate projection can bring both buyer and seller down in an avalanche of debt.”

“If projections are off by just a little, the consequences can be catastrophic; the margin for error is razor thin.”

It’s a reminder that when the stakes are high and leverage is maxed, the best defense is humility, discipline, and never assuming the numbers will break your way.

Tax maneuvers change the game

Underneath the surface of every big deal are the tax rules, and sometimes, a single loophole can be worth billions. In Barbarians at the Gate, creative financial engineering makes or breaks bids. A clever structure or a soon-to-expire tax provision isn’t just a rounding error; it’s the difference between winning and losing.

“It turned on an esoteric tax law loophole set to expire December 31, just two months away. In its first step, Finn’s plan called for First Boston to acquire RJR’s food businesses for a bundle of securities known as installment notes… The beauty of the idea was that, using the loophole, taxes on the notes could be deferred for ten or twenty years, creating a tax savings of as much as $4 billion.”

Timing and technical skill with the rules counted as much as any business analysis. Sometimes, financial engineering can create or destroy value, independent of how well or poorly the business itself is doing.

Who Is This For

I’ve read Barbarians at the Gate a couple of times now. The first time, I was a rookie in finance; eager, but with little context for what I was reading. Since then, after spending years studying Buffett, Munger, Singleton and others, I see the story differently. Experience helps you notice not just the numbers or the drama, but the underlying lessons about incentives, risk, and human nature.

At its heart, this book is about risk: how it’s packaged, traded, pushed around, and sometimes ignored. Strip away the jargon, and what you’re left with is a contest over who carries the downside when everyone wants the upside. LBOs are a bet that tomorrow’s cash will pay today’s bill. When that bet is wrong, the whole system can unravel in a hurry. The book shows, again and again, that for all the talk of financial engineering, nothing truly erases risk.

Who should read this? If you’re interested in business, investing, or the way real decisions get made when the stakes are highest, this is essential reading. It’s gripping as a story, but it’s better as a lens. Whether you’re a student, a professional, or just curious how fortunes are built and destroyed, Barbarians at the Gate will show you that the real levers in business aren’t always obvious, and sometimes, the biggest lessons are about what you can’t see coming.